In the modern age of digital banking, we’ve mastered the art of movement. We can flip between apps, settle invoices, and fund investment wallets with a speed that would have felt like magic twenty years ago.

But there is a dangerous trap hidden inside this efficiency: the belief that a high volume of activity is synonymous with wealth accumulation. We often mistake the “ping” of a notification for a step toward freedom, failing to realize that without building a financial structure, we are simply running on a treadmill that moves money around without letting any of it stick.

True prosperity isn’t found in the speed of your transfers; it is found in the integrity of your financial architecture. While most of the world is preoccupied with the binary choice of wealth vs transactions, the few who actually achieve lasting stability are those who treat their money as a project to be managed by a financial operating system.

Before you can grow your net worth, you have to stop the leakage that comes from uncoordinated movement and start designing the framework that allows your income to stay, compound, and eventually work for you.

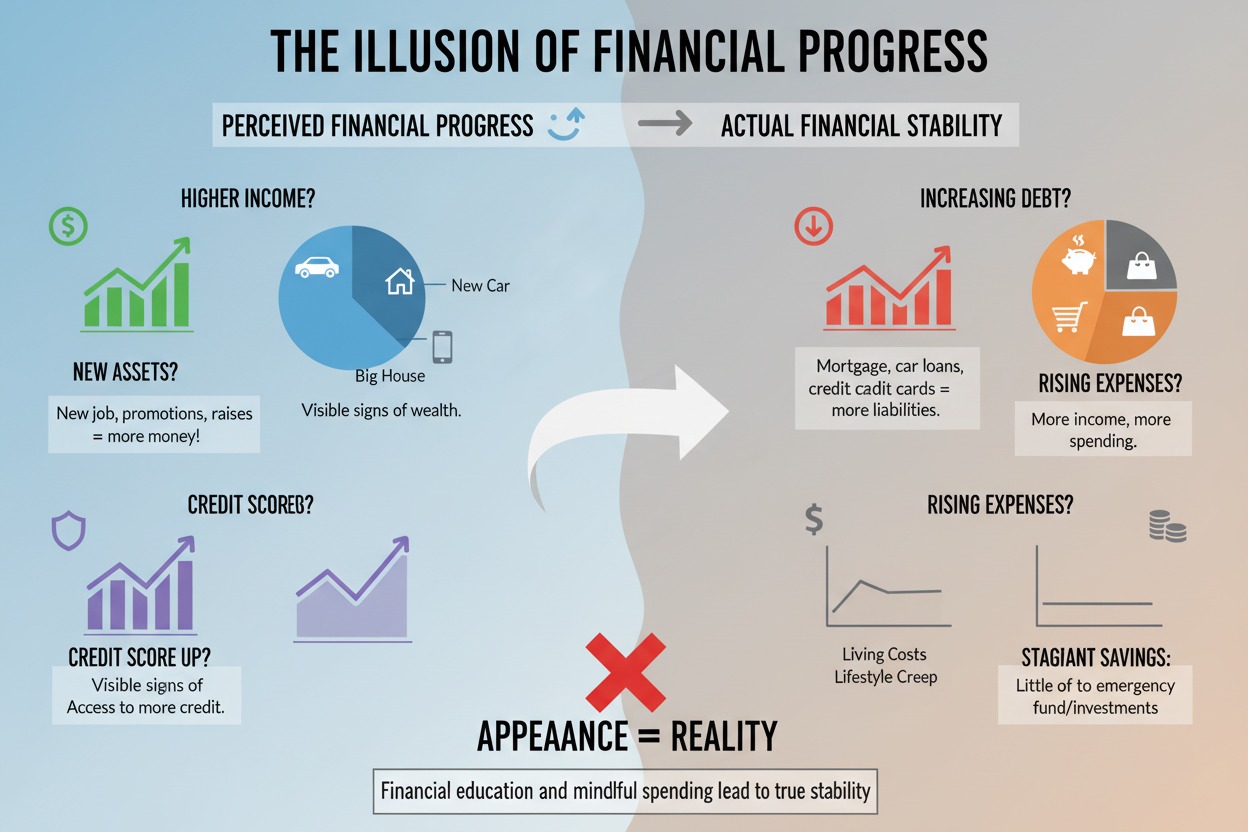

The Illusion of Financial Progress

We live in an era where money moves faster than ever before. With a few taps on a phone, salaries are paid, bills are settled, and transfers happen across multiple platforms in seconds. Digital banking and fintech innovations have made financial transactions incredibly convenient. Every day, millions of notifications pop up on our phones, letting us know that money has arrived, departed, or been redirected. From the outside, this constant movement gives the impression that real financial progress is happening. After all, the accounts are busy, and bank statements are filled with lines of activity.

Yet, beneath all this movement lies a quiet reality that many people only recognize much later: transactions move money, but they do not necessarily build wealth. For wealth to grow, something deeper than mere activity must exist. Wealth requires structure. Without that structure, money can circulate endlessly through your accounts without ever accumulating into something meaningful for your future.

The Cycle of Busy Finances

Consider the common story of a professional starting a new career. After years of school, that first salary feels like a major breakthrough. Suddenly, there is a reliable inflow of money every month, and life changes: better clothes, independent housing, and lifestyle upgrades become possible. The financial life becomes busy very quickly: salary arrives, bills are paid, and subscriptions renew automatically. The account balance gradually declines until the next payday, repeating a familiar rhythm.

If you look at a bank statement over a year, you might see thousands of transactions. But if you ask what actually accumulated from all that activity, the answer is often uncomfortable. Many professionals discover that despite years of steady income, their financial position has barely changed.

The problem isn’t a lack of hard work or even a lack of income; it’s that transactions alone do not create a financial structure. A transaction simply records that money moved; it doesn’t tell you if that movement actually made you stronger.

Why Activity Does Not Equal Wealth

Imagine someone earning ₦500,000 every month. On paper, that suggests stability. However, what matters is how that income flows through their personal system. Between rent, transportation, quiet subscriptions, and unexpected social obligations, the salary is often dispersed across dozens of obligations before the month is over. Before long, the financial life becomes a revolving door — income flows in, expenses flow out, and nothing stays long enough to grow or compound.

This same pattern appears frequently within businesses. A small company might generate millions in revenue, but if the business owner evaluates their personal net worth, they may find it hasn’t grown proportionally. The business generated activity, but it didn’t generate a structure to convert that revenue into personal assets.

Without a system, the company simply becomes a pipeline through which money travels rather than a foundation where wealth is built. This is why even businesses with impressive turnover can struggle to provide long-term security for their owners.

The Hidden Cost of Fragmented Finance

Another major obstacle to wealth today is fragmentation. Modern financial life is rarely centralized. A typical professional might have a salary enter one bank, use a fintech wallet for daily spending, keep savings in a separate app, and manage investments on another platform entirely. While these tools are useful, their independence means they rarely provide a unified view of a person’s financial health.

This fragmentation creates a subtle problem: people can see individual transactions, but they cannot see their complete financial architecture. They may know their balance in one account but not understand their total net worth or how their weekly spending compares to long-term goals. Without a unified view, financial decisions are made in isolation — one transaction at a time. Over years, this lack of visibility prevents people from recognizing whether their financial life is actually progressing or simply standing still.

Wealth Comes From Structure

Wealth does not emerge from random activity; it emerges from intentional structure. Individuals who build lasting stability design systems that determine how money behaves before it even arrives. They know exactly where income should go the moment it hits their account, separating spending from investment and monitoring how quickly debt shrinks. They operate within a framework that organizes their life, ensuring transactions serve a larger purpose of increasing net worth.

Shifting from “financial activity” to “financial architecture” is a transformative step. It involves moving away from reacting to income and toward asking deeper questions:

- How should this income be distributed?

- What boundaries prevent lifestyle inflation?

- What mechanisms ensure consistent growth?

When these questions are answered by a system rather than guesswork, clarity replaces confusion. Spending becomes intentional, and wealth begins to accumulate because financial movement finally has a direction.

The Idea Behind FINTEL Suite

The philosophy behind FINTEL Suite emerged from observing these exact challenges. It became clear that most professionals don’t lack tools — they have banks, apps, and spreadsheets — but they lack a central system to organize them into a coherent structure. FINTEL Suite acts as a financial operating system that sits above your existing tools, providing a single structured view of your net worth, income flow, and long-term decisions.

There is a powerful distinction here: movement is not the same as momentum. Transactions create movement, which keeps money circulating; structure creates momentum, which builds wealth over time. If you’ve ever wondered where your money went despite years of steady income, you likely don’t have a lack of activity — you have a lack of structure. You can begin to change that today by visiting fintelsuite.com and giving your money a system that knows exactly where it should go.